JobKeeper is a Federal Government subsidy paid to eligible businesses effected by COVID-19 to cover the costs of their employee’s wages.

Affected employers will be able to claim a fortnightly subsidy payment of $1,500 per eligible employee from 30 March 2020, for a maximum period of 6 months. This full amount of $1,500 must then be paid to all eligible employees, whether they are full time, part time or casuals.

How JobKeeper payments are made

- They are paid by the ATO within 14 days of month end.

- The first payment will be on 1 May 2020.

- The eligible payroll periods are every 14 days, commencing 30 March 2020.

- Monthly employer payroll reporting is required to trigger the payment by the ATO – using Single Touch Payroll (STP)

The employer will continue to receive the subsidy payments for eligible employees while they are eligible for the payments. While the program is expected to run for 6 months, payments will stop if the employee is no longer employed by the business.

Business Participation Entitlement

Sole traders and some other entities (such as partnerships, trusts or companies) may be entitled to the JobKeeper Payment scheme under the business participation entitlement. A limit applies of one $1,500 JobKeeper payment per fortnight for one eligible business participant. Sole traders, one partner in a partnership, one beneficiary of a trust, and one director or shareholder of a company may be regarded as an eligible business participant.

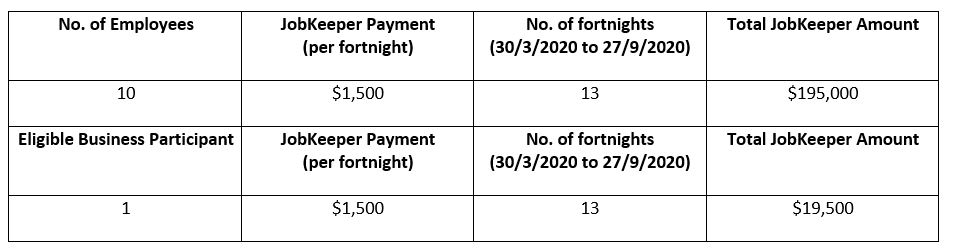

The Value of JobKeeper to business

Based on a business with 10 employees and provided they are eligible to receive the JobKeeper payment for all employees for the entire 6 month period, we estimated what the business will receive.

This is obviously a huge assistance during these difficult times.

Obligations and Risks for you

If a wrong claim is made or if the ATO in the future decides that you were ineligible to receive the JobKeeper payment, the ATO will require you to repay them any JobKeeper payments that you have received plus penalties and interest.

The key risks to you as the employer include:

- The employer certifies the facts provided to the ATO and the JobKeeper claim made.

- The employer receives significant JobKeeper payments over a 6 month period. For example, an employer with 10 employees would receive $195,000, and an employer with 20 employees would receive $390,000.

- If the employer makes a mistake and is found to be ineligible by the ATO (for example, its turnover is not down by 30%), then they may have to repay all amounts received back to the ATO.

- An employee ceases to be eligible if they cease employment during the life of this JobKeeper scheme.

Also, the ATO requires you to keep all records in relation to your JobKeeper claim for a 5 year period.

Our work plan to assist you

The ATO has specific actions that must take place within tight time frames for an employer to receive the JobKeeper payment. These are the actions that we can assist you with:

Employer Eligibility Assessment – NOW

- Review ATO requirements for the business

- Review ATO requirements for employees

- Review ATO requirements for Business Participation Entitlement – Sole Trader, Partnership, Company or Trust

- Document the fall in turnover % in case of future ATO audit

Identify Eligible Employees – NOW

- Prepare list of eligible employees

- Prepare JobKeeper employee nomination notice for all eligible employees and ensure all notices are signed

Make Correct Wage Payments to Eligible Employees – NOW

- Ensure your payroll software is correctly set up to record JobKeeper “top up” payments

- Pay the minimum $1,500 before tax to each eligible employee each fortnight (starting with the fortnight 30 March to 12 April) to be able to claim the JobKeeper payment for that fortnight

- Continue to pay the minimum $1,500 to employees in every subsequent fortnight until 27 September 2020

Enrolment for JobKeeper – From April 20

Enrol for JobKeeper using ATO online services from 20 April 2020:

- Provide employer bank account details for receipt of JobKeeper payment

- Confirm if applicant is entitled to a “Business Participation Payment”

- Specify the number of employees who will be eligible for one period and the number eligible for two periods

- Get confirmation that all employees the employer plans to nominate are eligible and the employer has notified them and has their agreement

Apply for JobKeeper Payments – From 4 May

- Apply to claim the JobKeeper payment using ATO online services between 4 May 2020 and 31 May 2020

- Ensure all eligible employees have been paid $1,500 per fortnight

- Identify the eligible employees from a STP prefill or by manually entering into ATO online services

- Update your accounting system Chart of Accounts to ensure JobKeeper payments are coded correctly

Monthly JobKeeper Declaration Report – Due by the 7th of each month

Using ATO online services, report to the ATO using their Monthly JobKeeper Declaration Report on the following:

- Reconfirm that your reported eligible employees have not changed

- Input current GST Turnover for the reporting month

- Input projected GST Turnover for the following month

- Notify if any eligible employees have changed or left your employment

We can help you

You have limited time to enrol you for JobKeeper (starting on 20 April 2020) and then making your first Application for JobKeeper Payments (starting on 4 May 2020). There is a lot of work we need to do for you so that you can potentially receive the maximum JobKeeper benefit, and we want to be as transparent as possible with you and can calculate a price for our services and advice. Please contact Stephanie on stephanie@rvpartners.com.au to receive an estimate.

We’ll send you our fee proposal for our services. Once we receive your signed proposal with payment, we will get your work completed. With our ongoing work, we will invoice you at the beginning of each month, we will then lodge your Monthly Job Keeper Declaration Report with the ATO.

General Advice Disclaimer: The information contained within this document is of a general nature only and neither represents nor is intended to be personal advice on any particular matter. Robinson Voss Partners (RV Partners) strongly suggests that no person should act specifically on the basis of the information in this document, but should obtain appropriate professional advice based on their own personal circumstances.